When people go into business together, they usually focus on growth, opportunity, and shared goals. Very few spend enough time planning for what happens if one partner can no longer continue due to death, disability, or an unexpected exit. Having insurance on key personnel is important, but it can be even more crucial for the business owners or partners.

That’s not pessimism, it’s responsible planning.

Buy–sell insurance is designed to protect the business, the remaining partners, and the family of the departing owner. When it’s set up properly, it can prevent confusion, conflict, and financial strain during an already difficult time.

What Is a Buy–Sell Agreement?

A buy–sell agreement is a legal contract that outlines what happens to a business owner’s shares if certain events occur, such as:

- Death

- Disability

- Retirement

- Voluntary exit

- In some cases, divorce or insolvency

The agreement typically specifies:

- Who can buy the departing owner’s shares

- How the business will be valued

- How the purchase will be funded

Without a buy–sell agreement, ownership transitions can become messy very quickly.

What Happens If a Partner Dies Without a Plan?

This is where many business owners are caught off guard.

Without a buy–sell agreement:

- The deceased partner’s shares often pass to their spouse or estate

- Remaining partners may suddenly be in business with someone who has no interest or experience

- The family may want cash, while the business can only offer equity

- Disputes and financial strain can threaten the survival of the company

Proper insurance planning exists to avoid these exact situations.

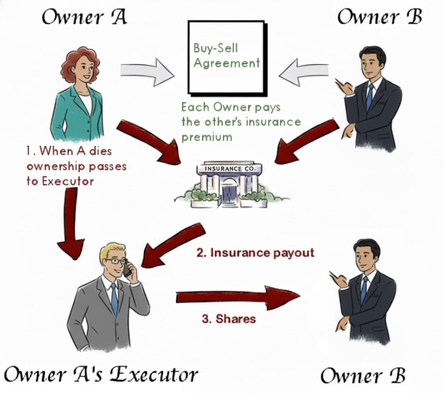

How Buy–Sell Insurance Fits In

A buy–sell agreement outlines what should happen. Buy–sell insurance provides the funding to make it happen.

In most cases, life insurance is used to fund the agreement. If a partner passes away:

- The insurance pays out

- The remaining partner(s) use the funds to buy the deceased partner’s shares

- The family receives fair value in cash

- Ownership stays with the remaining partners

This structure provides clarity and liquidity when it’s needed most.

Why Insurance Is Often the Funding Solution

There are other ways to fund a buy–sell agreement, such as borrowing or using retained earnings, but insurance is often preferred because:

- Immediate liquidity when it’s needed

- No debt added to the business

- Predictable and cost-effective

- Designed specifically for this purpose

Insurance allows business owners to plan for a major financial event without tying up operating capital.

Common Buy–Sell Insurance Structures

There are a few common ways buy–sell insurance can be structured in Canada:

- Cross-purchase: Partners own policies on each other

- Corporate-owned: The business owns the policies and redeems shares

- Hybrid structures: Used in more complex situations

The right structure depends on the business, number of partners, tax considerations, and long-term plans.

Why Buy–Sell Insurance Protects Families Too

This isn’t just about business continuity. It’s also about taking care of families.

For the departing owner’s family, buy–sell insurance:

- Provides fair value for their loved one’s ownership

- Avoids long delays or disputes

- Converts illiquid business shares into cash

- Reduces stress during an already emotional time

For many families, this clarity is just as important as the financial outcome.

When Should Business Owners Consider Buy–Sell Insurance?

Buy–sell insurance is especially important when:

- There are multiple owners or partners

- The business is privately held

- The company represents a large portion of personal net worth

- There is no clear succession plan yet

- Partners want certainty and fairness

The best time to plan is when everyone is healthy and aligned.

Final Thoughts

Buy–sell insurance isn’t about expecting the worst. It’s about protecting what you’ve built and the people who depend on it.

When ownership transitions are planned properly, businesses survive, partnerships remain intact, and families are treated fairly.

If you’re a business owner or partner and want to understand whether buy–sell insurance makes sense for your situation, I offer straightforward, no-pressure conversations to help you get clarity.

👉 Want to protect your business and your family? Book a free consultation today.